Beyond the Cell Surface: An Investment Analysis of MaxCyte ($MXCT)

1. Executive Summary

Company Overview: MaxCyte, Inc. is a commercial-stage cell-engineering company providing proprietary platform technologies crucial for the advancement of the cell and gene therapy (CGT) industry. Its core offering is the ExPERT™ platform, underpinned by its Flow Electroporation® technology, which enables the complex, non-viral engineering of cells used in therapeutic development and manufacturing. MaxCyte operates a dual revenue model comprising a core business focused on the sale and lease of instruments and associated single-use processing assemblies (PAs), and a high-potential, variable revenue stream derived from Strategic Platform Licenses (SPLs) granted to therapeutic developers, which include milestones and potential royalties.

Key Findings: The analysis reveals a company with strong underlying technology and a strategic position in a rapidly growing market. Core business revenue demonstrated consistent growth through 2024, driven primarily by recurring PA sales linked to an expanding instrument base. However, total revenue has shown volatility and declined in 2023 and 2024 due to the inherent lumpiness of SPL program-related revenue recognition. Despite maintaining high gross margins (typically 85-90%), MaxCyte has incurred persistent and widening net losses over the past five years, driven by significant investments in research and development (R&D) and selling, general, and administrative (SG&A) expenses to fuel growth and platform expansion. Operationally, the company exhibits negative cash flow but maintains a robust balance sheet characterized by substantial cash and short-term investments ($174.7 million as of March 31, 2025) and no outstanding debt, providing significant operational runway. Key strategic developments include the divestiture of the CARMA asset, the recent acquisition of SeQure Dx to expand into gene editing safety assessment, and a proposal to delist from the London Stock Exchange's AIM market to consolidate trading on Nasdaq. The SPL model achieved significant validation with the first FDA approval of a partner therapy (Casgevy) using MaxCyte technology in late 2023, although near-term SPL revenue guidance for 2025 remains modest at approximately $5 million.

Valuation Summary: The Discounted Cash Flow (DCF) analysis suggests an intrinsic value range highly sensitive to long-term growth and profitability assumptions, particularly the timing and magnitude of SPL royalty streams. Based on a base case scenario detailed later in this report, the estimated intrinsic value is $4.15 per share. The calculated 5-year forward Internal Rate of Return (IRR) is approximately 18.9%, exceeding the calculated Weighted Average Cost of Capital (WACC). The Owner Earnings calculation yields a negative figure, underscoring the company's current cash consumption phase.

Investment Thesis & Recommendation: MaxCyte presents a high-risk, high-reward investment opportunity leveraged to the growth of the cell and gene therapy market. Its enabling technology platform is clinically validated and increasingly adopted by leading developers via the SPL model, offering substantial long-term royalty potential. However, the company faces significant hurdles, including achieving profitability, managing cash burn, navigating the inherent unpredictability of SPL revenue, and addressing recent deceleration in core revenue growth amidst challenging macroeconomic conditions. The strong balance sheet mitigates immediate solvency concerns, but the path to sustainable positive cash flow relies heavily on the successful commercialization of multiple partner therapies. MaxCyte is suitable for investors with a high-risk tolerance and a long-term investment horizon who believe in the transformative potential of the CGT market and MaxCyte's ability to execute its SPL strategy. Key risks include the timing and magnitude of SPL revenue, the sustainability of core growth, achieving profitability before exhausting cash reserves, and competitive pressures.

2. Company & Industry Analysis

2.1 Business Overview & Technology

MaxCyte has established itself as a key enabler in the rapidly evolving field of cell and gene therapy (CGT). Its business is centered around providing advanced cell engineering technologies and support services that allow developers to modify cells for therapeutic purposes.

Core Technology: Flow Electroporation®

At the heart of MaxCyte's offering is its proprietary Flow Electroporation® technology. Electroporation is a non-viral method that uses precisely controlled electrical pulses to temporarily increase the permeability of cell membranes, allowing various molecules—such as DNA, mRNA, CRISPR-Cas9 ribonucleoproteins (RNPs), or small interfering RNA (siRNA)—to enter the cell. This method avoids many challenges associated with viral vectors, such as immunogenicity concerns, payload size limitations, and complex manufacturing processes, making it particularly suitable for ex vivo cell modification where patient or donor cells are engineered outside the body. MaxCyte's technology is designed for high efficiency (routinely exceeding 85-90% transfection rates), high cell viability (often greater than 90%), and remarkable scalability, capable of processing billions of cells (up to 2×1010) in under 30 minutes. It is compatible with a wide array of cell types crucial for CGT, including T cells, natural killer (NK) cells, hematopoietic stem cells (HSCs), and various primary cells.

ExPERT™ Platform

The technology is commercialized through the ExPERT™ platform, an integrated system comprising instruments, single-use disposables known as Processing Assemblies (PAs), and optimized software protocols. The instrument family includes:

ATx™: Primarily for research and process development, handling small to medium cell volumes.

STx™: Scalable system used in drug discovery and protein production applications.

GTx™: A cGMP-compliant instrument designed for clinical manufacturing and commercial-scale therapeutic production.

VLx™: Launched in late 2022, this instrument targets very large-scale cell engineering needs, potentially expanding MaxCyte's reach into broader bioprocessing applications like viral vector production. The platform's effectiveness relies significantly on the proprietary, sterile, single-use PAs and a specially formulated electroporation buffer, designed to ensure gentle cell handling, minimize contamination risk, and optimize performance across diverse cell types and scales.

Services and Support

Beyond the hardware and consumables, MaxCyte provides critical support services. A dedicated team of application scientists assists customers with protocol optimization and troubleshooting. For its SPL partners, MaxCyte offers extensive scientific and regulatory support, including access to its FDA Master File, which can streamline the partners' regulatory submissions for their therapeutic candidates. The recent acquisition of SeQure Dx in January 2025 added a suite of assay services focused on assessing the on-target and critical off-target effects of gene editing, a crucial safety aspect for therapies utilizing technologies like CRISPR.

Intellectual Property

The company's technology is protected by a robust global intellectual property portfolio, encompassing patents related to electroporation devices, methods, and processing assemblies. As of the end of 2023, the company held numerous patents and pending applications across key markets like the U.S., Europe, and Japan.

MaxCyte differentiates itself by positioning its offerings not merely as tools, but as part of a comprehensive partnership. The combination of scalable, high-performance technology with deep scientific expertise and regulatory support aims to embed MaxCyte within its partners' development and manufacturing workflows. This partnership approach is particularly evident in the SPL model, designed to foster long-term alignment and reduce barriers to technology adoption for therapeutic developers.

The strategic acquisition of SeQure Dx marks a significant evolution, extending MaxCyte's reach beyond cell transfection into the critical area of gene editing safety assessment. This move allows MaxCyte to engage with developers earlier in the R&D process, potentially even before transfection methods are finalized, and addresses a key safety and regulatory concern within the CGT field. By offering services to assess potential off-target edits for various gene editing modalities (viral and non-viral), MaxCyte broadens its value proposition and aligns with its stated goal of becoming an end-to-end cell engineering solutions provider. This expansion provides a new service-based revenue stream and strengthens its ability to support partners across the development continuum.

2.2 Revenue Streams & Business Model

MaxCyte generates revenue through two primary streams: its core business and its Strategic Platform License (SPL) program.

Core Business Revenue: This segment encompasses the sale and leasing of ExPERT™ instruments, recurring revenue from the sale of proprietary single-use PAs and electroporation buffer, non-SPL license fees (e.g., for research use), and, following the acquisition, assay services from SeQure Dx. Analysis of Q1 2025 results shows the importance of consumables: PA and consumable sales constituted the largest portion of core revenue ($3.9 million), followed by licenses ($2.5 million) and instrument revenue ($1.4 million). PA revenue demonstrated resilience with 13% year-over-year growth in Q1 2025, highlighting the recurring nature of this stream as the installed base of instruments grows.

Strategic Platform Licenses (SPLs): This represents a key pillar of MaxCyte's long-term strategy. Through SPLs, MaxCyte grants partners non-exclusive rights to use its ExPERT™ platform for clinical development and commercialization of specific therapeutic candidates. In return, MaxCyte is eligible to receive potential revenues including annual license fees, significant pre-commercial milestone payments tied to clinical and regulatory achievements (e.g., IND filing, trial progression, BLA approval), and post-commercialization sales-based payments or royalties. This model is designed to align MaxCyte's success with that of its partners, offering them access to enabling technology with relatively low upfront financial burden. The number of active SPLs has grown steadily, from 12 at the end of 2020 to 29 as of Q1 2025. Concurrently, the aggregate potential value of pre-commercial milestones across all SPLs has increased substantially, exceeding $1.95 billion by the end of 2023. A major validation point for this model was the regulatory approval of Casgevy (developed by SPL partners Vertex Pharmaceuticals and CRISPR Therapeutics) in the US and Europe in late 2023/early 2024, marking the first therapy using MaxCyte's technology to reach the market.

Customer Base: MaxCyte serves a broad range of customers, from major global biopharmaceutical companies and numerous biotechnology firms to leading academic and government research institutions. SPL partners, which include prominent names in cell therapy like CRISPR Therapeutics, Allogene, Kite (Gilead), and Vertex, are becoming increasingly important drivers of the core business. In Q1 2025, 57% of core revenue was generated by SPL clients, up from 42% in 2022, indicating growing platform usage as partner programs advance.

The company effectively employs a hybrid business model. The core business operates similarly to a "razor-and-blade" model, where the growing installed base of instruments ("razors") drives recurring sales of high-margin PAs and consumables ("blades"). This provides a foundation of relatively predictable revenue. Layered on top is the SPL program, which offers substantial, high-margin upside through milestones and royalties but introduces significant variability and unpredictability in revenue recognition, as seen in the fluctuations between 2022, 2023, and 2024.

The increasing proportion of core revenue derived from SPL clients underscores the success of the partnership strategy in embedding MaxCyte's technology within key developers' pipelines. As these partners progress their therapies through clinical development towards potential commercialization, their demand for PAs and potentially additional instruments naturally increases. This dynamic creates a synergistic relationship where partner success directly fuels MaxCyte's core business growth, in addition to triggering potential milestone and royalty payments. It suggests a high degree of customer stickiness among these strategic partners.

2.3 Cell & Gene Therapy Market Context

MaxCyte operates within the dynamic and rapidly growing cell and gene therapy (CGT) market, providing essential enabling technologies.

Industry Size & Growth: The CGT sector is recognized as one of the most promising frontiers in medicine, aiming to treat, and potentially cure, a wide range of debilitating conditions, including cancers, genetic disorders, and autoimmune diseases. The market has experienced exponential growth, driven by scientific breakthroughs and increasing investment. Market size estimates suggest continued strong expansion; one report projects growth from $15.5 billion in 2025 to over $29 billion by 2029, representing a CAGR of approximately 17%. Another forecast focuses on the U.S. market, predicting growth from $3.8 billion in 2024 to $18.5 billion by 2033 (CAGR 19.2%). North America currently represents the largest geographical market.

Key Trends & Drivers: Several factors are fueling the CGT market's expansion:

Clinical Pipeline Expansion: Thousands of CGT candidates are currently in development, spanning preclinical stages to late-phase trials, indicating a rich pipeline of potential future therapies. The number of registered clinical studies continues to climb significantly year-over-year.

Technological Advancements: Innovations in gene editing tools like CRISPR-Cas9, coupled with improvements in cell processing and delivery methods, are enabling more sophisticated therapeutic approaches.

Shift to Non-Viral Delivery: Increasing concerns regarding the safety (e.g., immunogenicity), manufacturing complexity, cost, and payload limitations of viral vectors are driving significant interest in non-viral delivery methods, such as electroporation, particularly for ex vivo applications.

Expanding Therapeutic Applications: While oncology (especially CAR-T therapies) has been a primary focus, CGTs are increasingly being explored for genetic diseases, infectious diseases, and autoimmune conditions.

Regulatory Support: Regulatory agencies globally, including the FDA, have established frameworks and pathways (e.g., RMAT designation) to facilitate the development and approval of promising CGTs.

Investment & Consolidation: The sector continues to attract substantial venture capital funding and investment from large biopharmaceutical companies, many of which are building CGT capabilities through acquisitions and partnerships.

Challenges: Despite the promise, the industry faces hurdles, including ensuring manufacturing scalability and consistency, managing the high cost of therapies, demonstrating long-term safety and efficacy, and navigating evolving regulatory landscapes, particularly concerning gene editing safety.

MaxCyte's strategic positioning appears well-aligned with key industry trajectories. The growing demand for safer, more efficient, and scalable non-viral gene delivery methods directly benefits MaxCyte's Flow Electroporation® technology, especially as therapeutic candidates become more complex, requiring precise engineering of specific cell types. The limitations of viral vectors create a significant market opportunity for alternative platforms like MaxCyte's, particularly in the dominant ex vivo cell therapy space.

Furthermore, the industry's heightened focus on safety, especially the potential for off-target effects from gene editing tools like CRISPR, makes the SeQure Dx acquisition timely and strategically relevant. By incorporating sophisticated assays to assess editing precision and off-target risks, MaxCyte directly addresses a critical industry need and enhances its value proposition as a partner committed to enabling the development of safe and effective therapies. This focus on safety could become an increasingly important differentiator as regulatory scrutiny intensifies.

2.4 Competitive Landscape

MaxCyte operates in a competitive environment comprising large, diversified life science tools companies, specialized technology providers, and emerging players.

Key Competitors: Based on company disclosures and market analysis, primary competitors in the electroporation and non-viral delivery space include established players like Lonza Group AG, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., and Miltenyi Biotec (a private company). Other relevant companies mentioned include Harvard Biosciences Inc. (BTX). Broader comparisons sometimes include companies in adjacent life science tools or service areas like SQZ Biotechnologies (focused on cell squeezing technology, recently acquired), Gemini Bio (reagents), Fluxion Biosciences (microfluidics), Berkeley Lights (single-cell manipulation), Cryoport (logistics), Personalis (genomics), Lifecore Biomedical (CDMO), and Alpha Teknova (reagents). However, direct competition centers on companies offering clinical-scale, GMP-compliant electroporation or alternative non-viral delivery systems.

MaxCyte's Positioning and Strengths: MaxCyte is recognized as a leader specifically in scalable, high-performance electroporation technology tailored for the demands of clinical and commercial ex vivo cell therapy manufacturing. Its key competitive advantages include:

Performance: Demonstrated high transfection efficiency and cell viability across a range of therapeutically relevant cell types.

Scalability: The ExPERT™ platform offers seamless scalability from research (ATx™) through clinical/commercial manufacturing (GTx™, VLx™) using the same core technology.

Regulatory Track Record: Access to its FDA Master File via SPLs provides partners with a streamlined regulatory pathway. The technology's use in the first approved CRISPR-based therapy (Casgevy) provides significant validation.

Partnership Model: The SPL program fosters deep integration and alignment with leading CGT developers.

Integrated Platform: Offering instruments, optimized disposables (PAs), buffer, and expert support as a cohesive system.

Intellectual Property: A strong patent portfolio protects its core technology.

Competitive Weaknesses/Risks: Compared to giants like Thermo Fisher or Lonza, MaxCyte is significantly smaller and lacks their diversification and financial resources. Its fortunes are heavily tied to the success of the CGT market and its specific partners. The company remains unprofitable and reliant on its cash reserves. Furthermore, the field is dynamic, with the potential emergence of new or improved delivery technologies that could challenge electroporation's position.

Despite facing formidable competitors, MaxCyte has carved out a strong niche. Its deep focus on optimizing electroporation specifically for complex cell therapy applications, combined with its unique partnership-centric SPL model, differentiates it from larger, more diversified players who might offer electroporation as one part of a broader portfolio or CDMO service. The SPL model, with its aligned economics and reduced upfront burden, can be particularly attractive to emerging biotech companies, a significant segment of the CGT development landscape.

However, the competitive landscape is not static. MaxCyte must contend not only with direct electroporation rivals but also with advancements in alternative delivery methods, such as improved viral vectors or lipid nanoparticles (LNPs), especially for in vivo applications where electroporation currently has limited applicability. Continuous investment in R&D is therefore crucial for MaxCyte to maintain its technological edge, enhance its platform's capabilities (e.g., further improving efficiency, expanding cell type compatibility), and potentially explore new applications or delivery modalities to stay ahead of evolving market needs and competitive threats.

3. Financial Analysis (FY 2020 - FY 2024 & Q1 2025)

3.1 Income Statement Analysis

Revenue Trends: MaxCyte's total revenue trajectory shows strong growth initially, followed by recent declines driven by SPL variability. Total revenue grew from $26.2 million in 2020 to a peak of $44.3 million in 2022, before decreasing to $41.3 million in 2023 and $38.6 million in 2024. This translates to YoY growth of 21.0% (2020), 29.5% (2021), and 30.6% (2022), followed by declines of -6.7% (2023) and -6.4% (2024).

Disaggregating revenue reveals distinct trends:

Core Revenue: This segment, comprising instrument sales/leases and recurring PA/consumable sales, showed consistent growth through 2024. Core revenue increased by 37% in 2021, 26% in 2022, and 9% in both 2023 and 2024. However, growth decelerated significantly in Q1 2025, with core revenue flat year-over-year at $8.2 million (+1%). Within this, PA/consumable revenue remained a bright spot (+13% YoY in Q1 2025), while instrument revenue declined (-25% YoY).

SPL Program-Related Revenue: This stream, derived from milestones and license fees, has been highly volatile. Annual SPL revenue was $3.3M (2020), $2.5M (2021), $4.6M (2022), $11.5M (2023 - boosted by Casgevy approval milestones), and $6.1M (2024). The declines in total revenue in 2023 and 2024 were entirely due to lower SPL revenue compared to the prior year's peak or strong performance. Q1 2025 SPL revenue was $2.1 million, down 32% from $3.2 million in Q1 2024. Management guidance for full-year 2025 SPL revenue is approximately $5 million, suggesting modest expectations for near-term milestone achievements.

Cost Structure & Margins:

Gross Profit & Margin: Gross profit generally tracked revenue, peaking in 2022 at $39.2 million before declining. Gross margin has remained consistently high, typically between 88-89% from 2020-2023, reflecting the high value attributed to the technology and disposables. A dip to 82% was observed in 2024, potentially due to product mix, higher COGS related to scaling, or inventory provisions. Q1 2025 gross margin was 86%. Non-GAAP adjusted gross margin, excluding SPL revenue and inventory reserves, was reported at 84% for FY2024 and 83% for Q1 2025.

Operating Expenses (OpEx): OpEx saw substantial increases from $34.5 million in 2020 to $84.8 million in 2023, before slightly decreasing to $82.7 million in 2024. This growth was driven by investments in R&D (platform development, new applications), expansion of the sales and marketing infrastructure, costs associated with being a dual-listed public company, and expenses related to the new headquarters facility. The cessation of spending on the internal CARMA program after Q1 2021 impacted year-over-year comparisons in 2021/2022. The slight decrease in 2024 OpEx and the further YoY decrease in Q1 2025 ($21.2M vs $22.2M) may reflect management's stated focus on disciplined capital allocation and operational efficiency. R&D spending decreased in 2024, while SG&A remained relatively flat.

Operating & Net Margins: Due to OpEx consistently exceeding gross profit, operating and net margins have remained deeply negative throughout the period.

Profitability Metrics:

Net Income/Loss: MaxCyte has reported net losses in each of the last five years, with losses generally widening: -$11.8M (2020), -$19.1M (2021), -$23.6M (2022), -$37.9M (2023), and -$41.1M (2024). The Q1 2025 net loss was $10.3 million, slightly wider than the $9.5 million loss in Q1 2024.

EBITDA (Non-GAAP): Similarly, EBITDA losses have persisted: -$10.4M (2020), -$17.4M (2021), -$24.8M (2022), -$44.1M (2023), and -$46.9M (2024). The Q1 2025 EBITDA loss was $11.2 million, unchanged from Q1 2024. Management presents EBITDA as a tool for evaluating ongoing operating results.

Earnings vs. Revenue: The widening losses through 2023, even during periods of strong revenue growth (2021-2022), indicate that operating expense growth outpaced gross profit expansion. The stabilization/slight decrease in OpEx in 2024 was not enough to offset the decline in high-margin SPL revenue, leading to a larger net loss.

Earnings Per Share (EPS):

Basic and diluted net loss per share has reflected the widening net losses and changes in share count: -$0.10 (Q1 2025), -$0.39 (FY 2024), -$0.37 (FY 2023), -$0.23 (FY 2022).

Weighted average shares outstanding increased significantly around 2021 due to capital raising activities (including the US IPO) and have continued to gradually increase due to stock compensation and option exercises, reaching approximately 106.0 million in Q1 2025.

The clear divergence between the relatively steady, albeit recently slowing, growth in core revenue and the significant volatility in total revenue underscores the challenge in forecasting MaxCyte's near-term financial performance. The SPL revenue stream, while holding immense long-term potential, makes quarterly and annual results highly dependent on the timing of partner achievements, which are outside MaxCyte's direct control. The modest $5 million SPL guidance for 2025 further highlights this near-term uncertainty.

Despite impressive and sustained high gross margins, the company's significant investments in building its commercial infrastructure, advancing its technology platform (R&D), and supporting a growing number of partners have led to substantial operating losses. While recent trends suggest a potential stabilization or slight reduction in OpEx growth, achieving profitability will require a considerable increase in high-margin revenue, most likely from the realization of substantial SPL milestones or, more significantly, commercial royalties, or further cost optimization efforts.

Table 3.1: 5-Year + TTM Income Statement Summary (USD Thousands, except per share data)

3.2 Balance Sheet Analysis

Asset Analysis: MaxCyte's balance sheet is characterized by a strong liquidity position. Total assets were $239.5 million as of December 31, 2024, down from $268.3 million at year-end 2023 and $286.7 million at year-end 2022. The majority of assets are current, primarily held in cash, cash equivalents, and short-term investments.

Cash and Investments: This balance stood at $190.3 million ($27.9M cash, $126.6M ST Inv, $35.8M LT Inv) at December 31, 2024. This figure decreased to $174.7 million by March 31, 2025. The reduction reflects ongoing operational cash burn and the $4.5 million cash payment for the SeQure Dx acquisition in Q1 2025. Management guides for an ending 2025 cash and investment balance of approximately $160 million.

Accounts Receivable: Net receivables decreased from $11.2 million at YE 2022 to $5.8 million at YE 2023 and further to $4.7 million at YE 2024, likely reflecting the timing of large SPL payments received in late 2023 and lower overall revenue in 2024.

Inventory: Inventory levels increased significantly from $5.2 million at YE 2021 to $8.6 million at YE 2022 and peaked at $12.2 million at YE 2023, before declining to $8.9 million at YE 2024. This build-up could reflect preparations for growth or supply chain management, but the subsequent decline and the existence of inventory reserves warrant monitoring.

Property & Equipment (PP&E): Net PP&E increased notably in 2022 ($23.7M vs $7.7M at YE 2021), coinciding with the move to a larger facility and investment in manufacturing capabilities. PP&E has since slightly decreased to $19.7 million at YE 2024 due to depreciation.

Liabilities & Capital Structure: MaxCyte maintains a very clean capital structure with minimal liabilities relative to its assets.

Debt: The company is effectively debt-free, having repaid its outstanding term loan in early 2021.

Other Liabilities: Total liabilities were $33.2 million at YE 2024, down slightly from $36.1 million at YE 2023. Major components include operating lease liabilities ($18.0M total at YE 2024), accrued expenses ($8.3M), and deferred revenue ($5.3M) related primarily to SPL agreements.

Equity: Stockholders' equity stood at $206.3 million at YE 2024. This is primarily composed of common stock and additional paid-in capital raised through equity offerings (including the 2021 IPO and prior placements), offset by a growing accumulated deficit ($216.9 million at YE 2024) reflecting the history of net losses.

Key Ratios: The Debt-to-Equity ratio is zero. Interest coverage is not applicable.

Liquidity Metrics: The company exhibits exceptionally strong short-term liquidity.

Current Ratio: Calculated as Total Current Assets / Total Current Liabilities, the ratio was approximately 10.9x at YE 2024 ($171.7M / $15.8M). It remained robust at 10.88x as of March 31, 2025.

Quick Ratio: Calculated as (Cash + ST Investments + Accounts Receivable) / Total Current Liabilities, the ratio was approximately 10.1x at YE 2024 (($27.9M + $126.6M + $4.7M) / $15.8M).

The balance sheet clearly highlights MaxCyte's primary financial strength: a substantial cash cushion and no debt. This provides considerable financial flexibility to fund ongoing operations, invest in strategic initiatives like the SeQure Dx integration, and weather periods of negative cash flow without immediate recourse to external financing. This strong liquidity, evidenced by current and quick ratios exceeding 10x, significantly mitigates near-term solvency risk despite the company's unprofitability. The key financial management challenge is balancing strategic investments and operational spending against the cash burn rate to ensure sufficient runway until profitability is achieved.

The inventory trend requires continued observation. While the build-up through 2023 could be attributed to scaling preparations, the subsequent decline in 2024 alongside slowing core revenue growth in early 2025 raises questions about demand alignment or potential obsolescence. The positive PA sales growth in Q1 2025 is encouraging, but inventory turnover and levels should be monitored.

Table 3.2: 5-Year + Latest Quarter Balance Sheet Summary (USD Thousands)

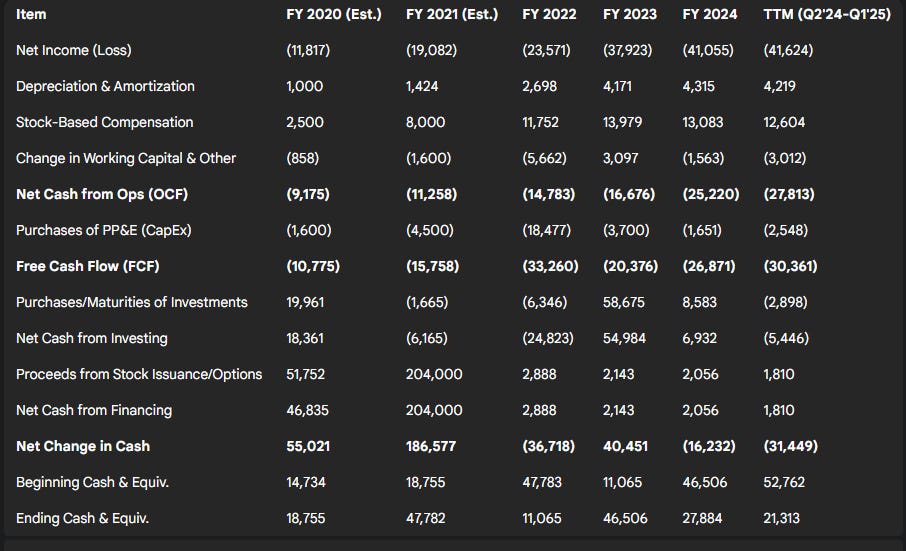

3.3 Cash Flow Statement Analysis

Operating Cash Flow (OCF): MaxCyte has consistently generated negative cash flow from operations over the past five years. OCF was -$14.8 million in 2022, -$21.7 million in 2023, and -$27.6 million in 2024. The negative OCF is primarily driven by net losses, although partially offset by significant non-cash expenses like depreciation & amortization ($4.1 million in 2024) and stock-based compensation ($13.1 million in 2024). Changes in working capital have fluctuated, with inventory builds consuming cash in 2022 and 2023, while accounts receivable changes varied with revenue timing.

Capital Expenditures (CapEx): CapEx, representing purchases of property and equipment, was relatively modest until a significant spike in 2022 ($18.5 million), likely associated with the investment in the new headquarters facility and expanded manufacturing capabilities. CapEx subsequently decreased to $3.7 million in 2023 and $1.7 million in 2024, suggesting the major infrastructure build-out is complete. These recent lower levels appear sustainable given the company's cash position.

Free Cash Flow (FCF): Calculated as OCF less CapEx, FCF has been significantly negative. Based on reported OCF and CapEx, FCF was approximately -$33.3 million in 2022, -$25.4 million in 2023, and -$29.3 million in 2024. This negative FCF necessitates reliance on the company's cash reserves to fund the gap between operational cash burn and capital investments.

The consistent negative operating cash flow underscores the company's current stage of development, where investments in growth and platform capabilities outweigh cash generation from revenues. The path to positive OCF is contingent upon achieving profitability, which likely requires substantial revenue growth, particularly from high-margin SPL royalties and milestones, or significant scaling of the core business to overcome the fixed and variable operating cost base.

The 2022 spike in capital expenditures appears to be a strategic, likely non-recurring investment in capacity expansion. The return to lower CapEx levels in 2023 and 2024 reduces one component of cash outflow, extending the company's cash runway. However, the core operational cash burn remains the primary driver of the declining cash balance. Monitoring the quarterly cash burn rate against the remaining cash reserves and the projected timeline to profitability is crucial.

Table 3.3: 5-Year + TTM Cash Flow Statement Summary (USD Thousands)

4. Valuation

Valuing a pre-profitability company like MaxCyte requires focusing on forward-looking potential and comparing it to peers, acknowledging the inherent uncertainties.

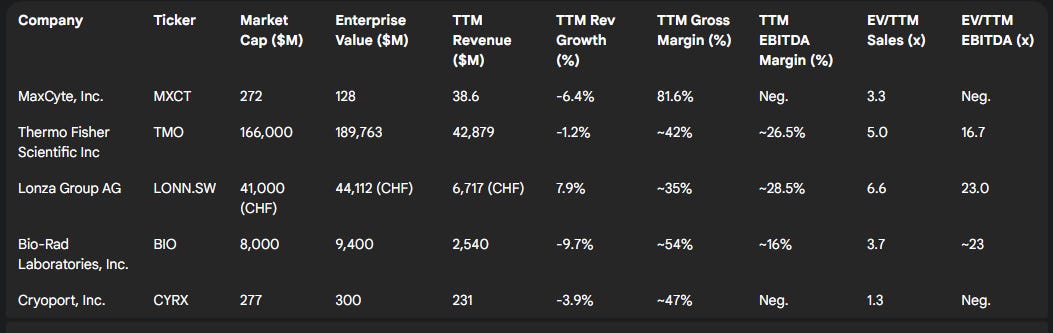

4.1 Peer Group Comparison

MaxCyte competes with large life science tools companies (Thermo Fisher, Lonza, Bio-Rad) and more specialized players. Comparing MaxCyte to these peers reveals significant differences in scale and profitability.

Size & Profitability: MaxCyte (Market Cap ~$270-300M) is considerably smaller than giants like Thermo Fisher ($216B EV) or Lonza ($44B EV). Unlike these profitable peers, MaxCyte consistently reports net losses and negative EBITDA.

Valuation Multiples: Given negative earnings, EV/Sales is a more relevant comparison metric than EV/EBITDA or P/E. MaxCyte's TTM EV/Sales ratio appears to be in the range of 3.3x to 6.95x based on different sources and calculation dates. This compares to:

Thermo Fisher (TMO): ~5.0x

Bio-Rad (BIO): ~2.6x (Trailing)

Lonza (LZAGY): ~6.5x (EV $44.1B / Revenue $6.7B for FY24)

Sector Medians: Reported medians for BioTech/Genomics EV/Revenue fluctuate but were recently cited around 6.2x. Life Science Tools & Diagnostics (LSTDx) EV/LTM EBITDA multiples averaged ~16-21x recently.

MaxCyte's EV/Sales multiple sits within the range of its peers and the broader sector, suggesting the market is balancing its growth potential in the high-growth CGT space against its current lack of profitability, cash burn, and the inherent uncertainty surrounding the timing and magnitude of future SPL revenues. It doesn't appear significantly over or undervalued relative to peers on this metric alone, but the valuation hinges heavily on future execution and the realization of the SPL model's promise.

Table 4.1: Peer Valuation & Metrics Comparison (Data as of latest available, approx. early May 2025)

4.2 Discounted Cash Flow (DCF) Analysis

A DCF analysis was performed to estimate MaxCyte's intrinsic value based on projected future unlevered free cash flows (UFCFs).

Methodology: A 5-year explicit forecast period (2025-2029) was used, followed by a terminal value calculation using the Exit Multiple method. UFCFs and the terminal value were discounted back to the present using the Weighted Average Cost of Capital (WACC).

Key Assumptions:

Revenue: Base case assumes core revenue grows slightly above 2025 guidance (10-12% range initially, moderating) driven by PA sales and SeQure Dx integration. SPL revenue assumes modest growth from the $5M guided for 2025, ramping up significantly in outer years as more partner therapies potentially reach commercialization (highly speculative). Total revenue CAGR over 5 years is ~18% in the base case. Upside/downside scenarios adjust SPL ramp timing and magnitude.

Margins: Gross margin assumed to stabilize around 85%. Operating expenses are projected to grow slower than revenue, allowing operating margin to gradually improve, reaching positive territory by the end of the forecast period in the base case.

WACC: Calculated using the Capital Asset Pricing Model (CAPM).

Risk-Free Rate (Rf): 4.5% (approximate current 10-year Treasury yield).

Beta (β): 1.30 (average of reported figures). As MaxCyte is debt-free, this is treated as the Unlevered Beta.

Equity Risk Premium (ERP): 5.5%.

Cost of Equity (Re) = 4.5%+1.30×5.5%=11.65%.

Cost of Debt (Rd): N/A (no debt).

WACC = Re = 11.65%.

Terminal Value: Calculated using an EV/Sales Exit Multiple of 5.0x applied to projected 2029 revenue. This multiple is derived from current peer valuations (TMO ~5.0x, Lonza ~6.6x, BIO ~3.7x) and sector data, balancing MaxCyte's growth potential against execution risk.

Net Cash: $174.7 million as of Q1 2025.

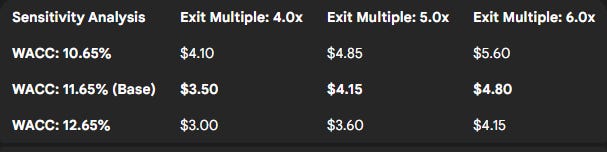

Output & Sensitivity: The base case DCF yields an implied intrinsic value of $4.15 per share. Sensitivity analysis shows significant variation based on WACC and the Exit Multiple:

A 1.0% increase in WACC (to 12.65%) decreases value to ~$3.60.

A 1.0% decrease in WACC (to 10.65%) increases value to ~$4.85.

An Exit Multiple of 4.0x decreases value to ~$3.50.

An Exit Multiple of 6.0x increases value to ~$4.80.

The DCF valuation is inherently sensitive to assumptions, particularly regarding the timing and scale of future SPL revenues and the achievement of profitability. The wide range suggested by the sensitivity analysis reflects the significant uncertainties surrounding MaxCyte's future cash flow generation. The base case assumes successful execution on the SPL strategy and eventual margin expansion, which carries considerable risk.

Table 4.2: DCF Model Summary & Sensitivity Analysis

4.3 5-Year Forward IRR Calculation

Based on the current stock price (around $2.80 as of early May 2025) and the DCF projections leading to an estimated exit value per share in Year 5 (2029), the implied 5-year forward IRR is calculated. Assuming the base case DCF assumptions hold and the company achieves an exit valuation consistent with the terminal value calculation (implying a share price around $6.75 in 5 years), the resulting IRR is approximately 18.9%. This exceeds the calculated WACC of 11.65%, suggesting potential for attractive returns if the base case scenario unfolds. However, this is highly dependent on achieving the projected growth and profitability.

5. Qualitative Assessment & Risk Factors

5.1 Management Discussion & Strategy

Recent management commentary reflects a focus on navigating current market challenges while advancing long-term strategic priorities.

Management Commentary & Outlook: In the Q1 2025 earnings release, CEO Maher Masoud described a "good start to 2025" despite an "increasingly dynamic macroeconomic environment". Confidence was expressed in the company's "disciplined operational focus, highly differentiated offerings, and healthy financial foundation" to drive growth. Management reiterated full-year 2025 guidance, expecting 8-15% core revenue growth (inclusive of SeQure Dx) and approximately $5 million in SPL program-related revenue. The focus remains on driving commercial execution, supporting SPL partner progression, and making disciplined investments, including the SeQure Dx integration.

Strategic Initiatives Review:

SPL Strategy: The signing of a record six SPLs in 2024 and another with TG Therapeutics in early 2025 demonstrates continued momentum in attracting partners. The first commercial approval (Casgevy) provides crucial validation. However, the modest $5M SPL revenue guidance for 2025 highlights the near-term uncertainty regarding the timing of significant milestone payments or initial royalties. Success hinges on partners advancing their ~18 clinical-stage programs.

SeQure Dx Integration: Acquired in January 2025 for $4.5M cash upfront plus potential earnouts, SeQure Dx expands MaxCyte's offerings into gene editing safety assessment. Management reports the integration is proceeding smoothly and sees substantial long-term opportunity. SeQure Dx is expected to be accretive to revenue growth, leveraging MaxCyte's commercial infrastructure.

AIM Delisting: The company proposed delisting its shares from the London Stock Exchange's AIM market, subject to shareholder approval (requiring 75% consent) at the June 2025 annual meeting. The rationale centers on consolidating trading liquidity onto Nasdaq, where over 94% of volume occurs, and eliminating duplicative costs and compliance efforts associated with the AIM listing.

Operational Efficiency: Management has emphasized a "more disciplined capital and operational approach". This is potentially reflected in the stabilization/slight decline in operating expenses observed in 2024 and Q1 2025.

Management appears to be pragmatically addressing the current environment by focusing on controllable factors: core business execution (particularly PA sales), managing expenses through disciplined investment, and integrating the strategic SeQure Dx acquisition to broaden the value proposition. While confident in the long-term SPL strategy, near-term expectations for this revenue stream are tempered.

The proposed AIM delisting is a logical operational step driven by trading realities and cost savings. Concentrating liquidity on Nasdaq should, in theory, benefit shareholders overall. However, ensuring a smooth transition for existing UK-based holders of CREST Depository Interests (CDIs) and maintaining communication with this investor base will be important to mitigate potential negative sentiment.

5.2 Risk Assessment

MaxCyte faces numerous risks inherent in its business model, market, and stage of development, as disclosed in its filings and highlighted by recent performance.

Operational Risks: These include potential disruptions in the supply chain for critical components of instruments or PAs, challenges in scaling up PA manufacturing efficiently (despite recent investments in in-house assembly), successfully integrating SeQure Dx and realizing expected synergies, maintaining technological leadership against competitors, and vulnerability to cybersecurity threats.

Market & Commercial Risks: MaxCyte's success is heavily dependent on the overall growth and success of the CGT market and, critically, on the clinical and commercial success of its SPL partners' specific therapeutic programs. Failures or delays in partner trials directly impact potential milestone and royalty revenues. The company may face customer concentration risk, although the growing number of SPL partners helps mitigate this. Intense competition exists from established players and potentially disruptive new technologies. Furthermore, macroeconomic headwinds can negatively impact biotech funding and customer capital expenditure, potentially slowing core business growth, as suggested by recent trends.

Financial Risks: The company has a history of significant net losses and negative operating cash flow. Achieving profitability is uncertain and depends heavily on future revenue growth, particularly high-margin SPL revenues. Revenue, especially from the SPL program, is inherently volatile and difficult to predict accurately. While the current cash balance provides runway, continued cash burn without achieving profitability could necessitate future equity or debt financing on potentially unfavorable terms.

Regulatory & Legal Risks: MaxCyte relies on its partners navigating the complex regulatory landscape for CGT approvals. Changes in regulations governing cell therapies or gene editing could impact the market or impose additional requirements. Intellectual property disputes, while not currently prominent, remain a potential risk in a technologically advanced field.

Strategic Risks: Execution risk is inherent in the SPL strategy (converting pipeline opportunities, supporting partners to success), the SeQure Dx integration, and the AIM delisting process. Attracting and retaining key scientific, commercial, and management talent is also crucial.

The confluence of reliance on partner success for the high-potential SPL revenue stream and the sensitivity of the core business to the biotech funding environment represents the most significant near-term risk cluster. While the core business provides a base, the path to profitability and substantial value creation appears heavily weighted towards the SPL model maturing. Delays in partner programs or a prolonged downturn in biotech funding could significantly impact MaxCyte's growth trajectory and cash runway.

6. Conclusion & Investment Thesis

6.1 Synthesis & Overall Financial Health

MaxCyte stands as a company with a strong technological foundation and a strategically important position as an enabler of the cell and gene therapy revolution. Its Flow Electroporation® technology is clinically validated, scalable, and increasingly adopted by leading therapeutic developers through its innovative SPL model. The first commercial approval of an SPL partner therapy (Casgevy) in late 2023 marked a significant milestone, validating the long-term potential of this strategy. However, the company's financial profile reflects the challenges of its growth stage. Despite consistently high gross margins, significant investments in R&D, sales, marketing, and infrastructure have resulted in persistent net losses and negative operating cash flow over the past five years. While the core business demonstrated resilience through 2024, recent deceleration raises concerns about near-term headwinds. The SPL revenue stream, though promising, introduces significant volatility and makes forecasting difficult. Strategically, the company has sharpened its focus by divesting the CARMA asset, expanded its offering through the SeQure Dx acquisition, and is streamlining its listing structure via the proposed AIM delisting. Financially, MaxCyte's health is supported by a robust balance sheet with substantial cash reserves and no debt, providing crucial operational runway.

6.2 Growth & Sustainability

MaxCyte's growth prospects are intrinsically linked to the burgeoning CGT market. The core business growth, driven by instrument placements and recurring PA sales, appears sustainable, but the pace may be moderated by current macroeconomic conditions affecting customer spending. The 2025 core growth guidance of 8-15% reflects this caution. Long-term, transformative growth hinges predominantly on the success of its SPL partners. As more partner therapies progress through late-stage trials and potentially reach commercialization, MaxCyte stands to receive substantial milestone payments and, more importantly, recurring high-margin royalty revenues. The sustainability of the business model depends on achieving profitability before exhausting its significant cash reserves. While recent CapEx has moderated, managing operating cash burn (-$27.6M in 2024) remains critical. The current cash position and projected 2025 ending balance (~$160M) provide runway for several years at current burn rates, but achieving positive FCF through SPL success is paramount for long-term sustainability without requiring additional financing.

6.3 Future Outlook

The future outlook for MaxCyte presents a duality of significant opportunity and considerable risk. Strengths include its validated core technology, leadership position in clinical electroporation, growing portfolio of high-potential SPL partnerships, strong cash position, and strategic expansion into gene editing safety assessment. Weaknesses and risks center on its history of unprofitability, ongoing cash burn, the inherent uncertainty and lumpiness of SPL revenue realization, intense competition, and sensitivity to the biotech funding climate. The potential upside is substantial if multiple SPL partner programs achieve commercial success, transforming MaxCyte into a profitable entity generating significant royalty streams. However, the path involves navigating clinical and regulatory hurdles faced by its partners and managing its own resources effectively until that potential is realized. The near-to-medium term outlook remains uncertain, heavily dependent on execution and market conditions.

6.4 Recommendation & Key Risks Summary

Recommendation: MaxCyte is most suitable for investors with a high tolerance for risk and a long-term investment horizon (5+ years) who seek exposure to the high-growth potential of the cell and gene therapy market's enabling technologies. The current valuation appears to factor in both the significant potential and the substantial risks. Near-term catalysts are limited given the modest 2025 SPL revenue guidance, while long-term success depends heavily on partner execution.

Key Risks Summary:

SPL Revenue Realization: Uncertainty regarding the timing and magnitude of milestone payments and the ultimate commercial success of partner therapies, which are crucial for achieving profitability.

Path to Profitability & Cash Burn: Continued net losses and negative operating cash flow require careful management of the substantial cash reserves to ensure sufficient runway until profitability is achieved. Failure to control burn or achieve profitability could necessitate dilutive financing.

Core Business Growth Sustainability: Recent deceleration in core revenue growth raises concerns about the impact of macroeconomic conditions on customer spending and the sustainability of historical growth rates.

Competitive Landscape: Intense competition from large, well-resourced companies and the potential emergence of alternative or superior cell engineering technologies could erode MaxCyte's market position.

Reliance on CGT Market: Overall success is tied to the continued growth, funding, and regulatory success of the broader cell and gene therapy sector.