Teva's Pivot: Charting a New Course for Growth in Pharmaceuticals

Buy

1. Summary

Teva Pharmaceutical Industries Ltd. (TEVA) is navigating a significant transformation, shifting from its historical identity as primarily a generics manufacturer towards a more balanced biopharmaceutical company with an increasing emphasis on innovative medicines. This strategic reorientation, termed the "Pivot to Growth," is central to Teva's current operational focus and future financial aspirations. As of the first quarter of 2025, Teva has reported its ninth consecutive quarter of revenue growth, signaling early positive momentum from this strategy.

Financially, Teva has demonstrated recent top-line expansion, driven by strong performance in its key innovative products—AUSTEDO, AJOVY, and UZEDY—which are collectively experiencing robust growth and are crucial to offsetting declines in mature product lines and the inherent pressures within the global generics market. While the company has made strides in improving its non-GAAP operating margins and has articulated clear targets for further margin expansion and free cash flow generation by 2027 and 2030, significant debt levels remain a key characteristic of its balance sheet, albeit with active management and recent credit rating upgrades.

The "Pivot to Growth" strategy is multifaceted, focusing on delivering growth from its current innovative portfolio, accelerating its late-stage pipeline, sustaining its generics and biosimilars business, and optimizing its overall business structure, including the planned divestiture of its API segment. The success of this strategy, particularly the clinical and commercial outcomes of its pipeline assets such as duvakitug and olanzapine LAI, represents a critical determinant of Teva's future value.

The valuation, incorporating a Discounted Cash Flow (DCF) model, an Owner Earnings assessment, and a 5-year forward Internal Rate of Return (IRR) projection, suggests a potential undervaluation at the current market price, contingent on successful strategy execution. Significant risks include the inherent uncertainties of pharmaceutical R&D, intense competition in both generics and innovative segments, and the successful continued management of its debt burden.

2. Get Oriented: Business & Industry Overview, Context Setting

Teva Pharmaceutical Industries Ltd. has a long-standing history in the pharmaceutical sector, having been incorporated in Israel in 1944, listed on the Tel Aviv Stock Exchange (TASE) in 1951, and later achieving a NASDAQ IPO in 1987 before moving to the New York Stock Exchange (NYSE) in 2012. This extensive operational history has positioned Teva as a major global player, traditionally known as a "generics powerhouse". However, the company is currently in a defined phase of strategic evolution.

Teva's Evolving Business Model

Teva's contemporary business model is characterized by a dual focus: maintaining its significant presence in the global generics market while concurrently expanding its portfolio of innovative pharmaceutical products. This strategic balance is designed to leverage the cash-generating capabilities of its established generics business to fund the research, development, and commercialization of higher-margin innovative therapies.

Revenue is primarily generated through three streams:

Generic Products: This includes a vast portfolio of generic prescription medications, over-the-counter (OTC) products, and increasingly, biosimilars. In 2024, generic medicines accounted for 57.2% of total revenues.

Innovative Products: This segment is spearheaded by key growth drivers such as AUSTEDO (for movement disorders), AJOVY (for migraine prevention), and UZEDY (for schizophrenia).

API (Active Pharmaceutical Ingredients): Teva has historically operated a significant API business. However, as part of its strategic refocusing, this segment is slated for divestiture to allow for greater concentration on core pharmaceutical operations.

Geographically, Teva operates and reports its financials across three main segments: the United States, Europe, and International Markets (which includes Canada, Israel, and other global territories).

"Pivot to Growth" Strategy - Deep Dive

Announced in May 2023, the "Pivot to Growth" strategy is the central framework guiding Teva's current and future operations. It is structured around four key pillars:

Delivering on Growth Engines: Maximizing the commercial potential of existing innovative products (AUSTEDO, AJOVY, UZEDY) and late-stage biosimilars.

Stepping Up Innovation: Accelerating the development of promising assets within its late-stage innovative pipeline.

Sustaining Generics Powerhouse: Maintaining a strong global commercial footprint, a focused portfolio and pipeline, and an efficient manufacturing network for its generic medicines.

Focusing the Business: Optimizing the overall product portfolio and global manufacturing footprint. This includes the strategic decision to divest the Teva API (Active Pharmaceutical Ingredients) business to concentrate resources on core areas of growth and innovation.

As of early 2025, Teva has reported the completion of Phase 1 of this strategy, termed "Return to Growth," marked by nine consecutive quarters of revenue growth. The company is now entering the "Acceleration Phase," aiming to build on this momentum.

Key financial targets associated with this strategy include achieving a 30% non-GAAP operating profit margin by 2027, generating free cash flow exceeding $2.7 billion in 2027 and over $3.5 billion by 2030, reducing net debt to 2x net EBITDA, and realizing approximately $700 million in net savings through organizational modernization and operational efficiencies.

The consistent articulation of the "Pivot to Growth" strategy in company communications underscores its critical importance. The market's perception of Teva and its valuation are now heavily dependent on the successful execution of this strategy and the achievement of its associated milestones. Any significant setbacks or failures in delivering on these strategic pillars could disproportionately affect investor confidence and the company's financial trajectory.

The divestiture of the API business, while aligning with the "Focusing the Business" pillar and potentially freeing up capital for R&D or debt reduction, may create near-term revenue adjustments and requires careful management to ensure a smooth transition without disrupting any internal supply synergies or the realization of expected financial benefits.

Pharmaceutical Industry Dynamics

The global pharmaceutical industry is characterized by several key dynamics. The branded drug sector faces ongoing pressures from patent expiries and the subsequent entry of generic and biosimilar competition. Generic markets, while offering volume, are marked by intense price competition and margin erosion. Biosimilar adoption is growing but varies by region and molecule. Across the board, pharmaceutical companies navigate complex regulatory environments, stringent drug approval processes, and increasing scrutiny on pricing and reimbursement from payors worldwide. R&D productivity and the ability to bring novel, differentiated therapies to market are critical for long-term success, especially as healthcare systems demand greater value.

Teva's Market Position, Strengths, and Weaknesses

Teva possesses several strengths, including its significant global scale as one of the largest pharmaceutical companies, a leading position in the global generics market, a growing portfolio of innovative products with demonstrated market traction, and an established commercial and manufacturing infrastructure worldwide.

However, the company also faces challenges. Historically, Teva has carried a substantial debt burden, largely a legacy of past acquisitions. While this is being actively managed and reduced, it remains a key financial consideration. The company has also navigated reputational challenges, including significant legal settlements related to opioid litigation. The success of its "Pivot to Growth" strategy is not guaranteed and carries inherent execution risks. Furthermore, the competitive pressures in both the generics and innovative drug markets are intense, requiring continuous adaptation and effective product lifecycle management.

The shift from a primary focus on high-volume, lower-margin generics to a more balanced model incorporating higher-margin, R&D-intensive innovative products is a fundamental change. This transition, while offering the potential for enhanced profitability and growth, also introduces a different risk profile, as success becomes more dependent on the outcomes of clinical trials and the successful commercialization of new, often complex, therapies.

3. Income Statement

An examination of Teva's income statement over the past five fiscal years and the most recent quarterly results reveals a company in transition, with emerging signs of success from its strategic pivot.

Revenue Trends

Overall revenues for Teva reached $16.54 billion in fiscal year 2024, an increase of 4% in U.S. dollars, or 6% in local currency terms, compared to 2023. This growth trend continued into the first quarter of 2025, with revenues of $3.9 billion, representing a 5% increase in local currency terms compared to Q1 2024. This marked the ninth consecutive quarter of revenue growth, a key indicator of the "Pivot to Growth" strategy gaining traction.

Segmental Performance: The United States segment has been a significant contributor to this growth, with Q1 2025 revenues reaching $1.91 billion, an 11% increase year-over-year, driven by both innovative products and generics. The generics business also showed positive momentum globally in Q1 2025, with growth in the U.S. (+5% LC), Europe (+1% LC), and International Markets (+2% LC).

Key Product Performance:

AUSTEDO: This innovative product for movement disorders continues to be a primary growth engine. Worldwide revenues for AUSTEDO reached $411 million in Q1 2025, a 39% increase in local currency compared to Q1 2024. Teva has raised its full-year 2025 revenue outlook for AUSTEDO to $1.95-$2.05 billion. In 2024, AUSTEDO generated $1.688 billion. The company targets AUSTEDO sales to exceed $2.5 billion by 2027 and $3 billion by 2030.

AJOVY: Global revenues for this migraine prevention treatment were $139 million in Q1 2025, up 26% in local currency. The 2025 revenue outlook is reaffirmed at approximately $600 million. AJOVY's 2024 revenues were $507 million.

UZEDY: Launched in 2023 for schizophrenia, UZEDY is showing strong early momentum with global revenues of $39 million in Q1 2025. Its 2024 revenues were $117 million. UZEDY, along with the pipeline asset olanzapine LAI, forms Teva's long-acting injectable (LAI) schizophrenia franchise, which has a peak sales potential estimated at $1.5-$2.0 billion.

Generics: The global generics business, including OTC and biosimilars, achieved revenues of $9.461 billion in 2024, an 11% increase from the prior year. This performance underscores the continued importance of this segment.

COPAXONE: Revenues from this mature multiple sclerosis product have continued to decline, as expected, due to generic competition.

The consistent and strong growth of these innovative products is crucial as it is successfully offsetting the revenue declines from mature products like COPAXONE and providing the main impetus for Teva's recent overall top-line recovery. This directly validates the initial successes of the first pillar of the "Pivot to Growth" strategy, which focuses on delivering from current growth engines.

Cost Structure & Margins

Gross Profit & Margin: Teva's GAAP gross profit margin was 48.2% in Q1 2025, an improvement from 46.4% in Q1 2024. The non-GAAP gross profit margin also improved to 52.8% in Q1 2025 from 51.4% in the prior-year quarter. For the full year 2024, the GAAP gross profit margin was 48.7%, up from 48.2% in 2023. This margin expansion is largely attributable to a favorable product mix, with a greater contribution from higher-margin innovative products.

Operating Expenses:

Research and Development (R&D): R&D expenses were $247 million in Q1 2025, a slight increase from Q1 2024, reflecting increased investment in immunology, immuno-oncology, and late-stage neuroscience projects. For FY 2024, R&D expenses were $998 million. As a percentage of revenue, R&D spending remains a critical area to monitor relative to pipeline progression.

Selling, General & Administrative (SG&A): In Q1 2025, Selling and Marketing (S&M) expenses were $622 million, and General and Administrative (G&A) expenses were $297 million. For FY 2024, S&M expenses were $3.009 billion, and G&A expenses were $1.009 billion. These costs are being managed alongside targeted savings programs.

Profitability Metrics

Operating Income & Margin: Teva reported GAAP operating income of $519 million in Q1 2025, a significant turnaround from an operating loss of $218 million in Q1 2024. The GAAP operating margin was 13.3% in Q1 2025. Non-GAAP operating income in Q1 2025 was $946 million, with a non-GAAP operating margin of 24.3%, up from 23.4% in Q1 2024. This improvement, even with increased R&D and S&M spending to support growth, points towards effective cost discipline and the positive impact of the shifting product mix. For FY 2024, Teva reported a GAAP operating loss of $303 million. The company is targeting a 30% non-GAAP operating margin by 2027. If the current trends in innovative product sales growth and cost management persist, this target appears increasingly attainable.

Net Income (Loss) Attributable to Teva: Net income was $214 million in Q1 2025. For FY 2024, Teva reported a net loss of $1.639 billion, compared to a net loss of $559 million in 2023. These figures have been impacted by various factors including impairments, legal settlements, and tax provisions.

Earnings Per Share (EPS)

In Q1 2025, GAAP diluted EPS was $0.18, and non-GAAP diluted EPS was $0.52.

For FY 2024, GAAP diluted EPS was a loss of $1.45, while non-GAAP diluted EPS was $2.49.

2025 Full Year Outlook (Revised): Teva updated its 2025 outlook, projecting revenues of $16.8-$17.2 billion, non-GAAP operating income of $4.3-$4.6 billion, adjusted EBITDA of $4.7-$5.0 billion, and non-GAAP diluted EPS of $2.35-$2.65.

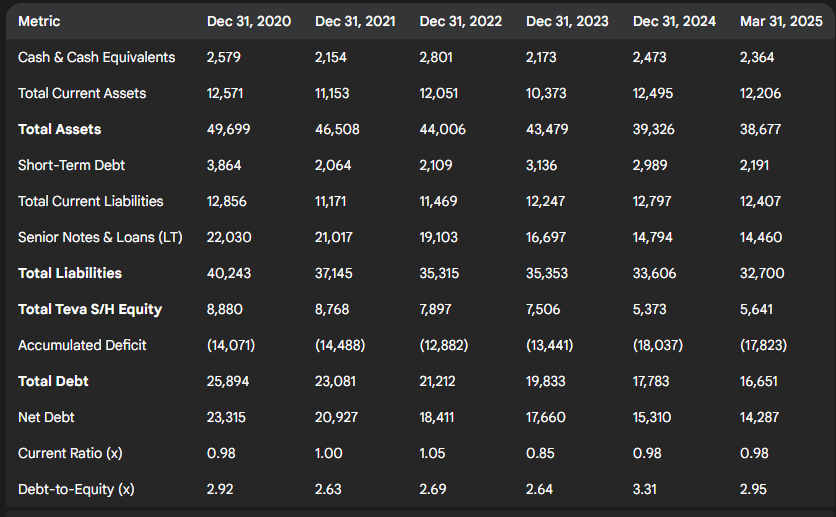

4. Balance Sheet

Teva's balance sheet reflects its history of significant acquisitions, ongoing efforts to manage its debt profile, and the financial impact of its strategic transformation.

Asset Analysis

Cash and Cash Equivalents: As of December 31, 2024, Teva held $2.473 billion in cash and cash equivalents, an increase from $2.173 billion at year-end 2023. As of March 31, 2025, cash and cash equivalents were $2.364 billion.

Accounts Receivables & Inventories: Accounts receivables, net, stood at $3.610 billion at December 31, 2024, while inventories were $3.991 billion. These levels are critical for managing working capital efficiency. As of March 31, 2025, accounts receivable were $3.595 billion and inventories were $4.013 billion.

Property, Plant & Equipment, Net (PP&E): Net PP&E was $5.493 billion at the end of 2024, reflecting ongoing investments and depreciation. This decreased to $5.403 billion by March 31, 2025.

Goodwill & Intangible Assets: These remain substantial components of Teva's asset base, primarily stemming from past acquisitions. As of December 31, 2024, goodwill was $16.681 billion, and identifiable intangible assets were $9.322 billion. By March 31, 2025, goodwill was $16.661 billion and identifiable intangibles were $9.029 billion. The company has a history of significant impairment charges related to these assets; cumulative goodwill impairment reached approximately $21.0 billion by June 2019 and $28.3 billion by March 2024. The considerable carrying values of goodwill and intangible assets continue to pose a risk. Should the future cash flows anticipated from the businesses or assets to which these are attributed not materialize as expected under the "Pivot to Growth" strategy, further impairment charges could negatively impact reported net income and shareholder equity.

Liabilities & Capital Structure

Debt Profile: Teva's total debt as of March 31, 2025, was $16.651 billion. At December 31, 2024, short-term debt (including current portion of long-term debt) was $2.989 billion, and senior notes and loans (long-term) amounted to $14.794 billion, totaling $17.783 billion. This is a reduction from $19.833 billion at year-end 2023.

Debt Reduction Progress: Teva is actively working to reduce its debt burden, with a stated target of achieving a net debt to adjusted EBITDA ratio of 2x. Recent activities include debt tender offers and the issuance of new senior notes, aimed at optimizing its maturity profile and reducing interest costs. These actions, coupled with improved credit ratings—Fitch upgraded Teva to BB+ in May 2025, and Moody's upgraded to Ba1—signal enhanced financial management and increasing market confidence. This improved financial flexibility is vital for supporting the capital-intensive R&D programs for its innovative pipeline.

Equity: Teva shareholders' equity was $5.373 billion as of December 31, 2024, with an accumulated deficit of $18.037 billion. By March 31, 2025, Teva shareholders' equity was $5.641 billion, and the accumulated deficit was $17.823 billion. The large accumulated deficit reflects past losses and impairment charges.

Liquidity Metrics

Current Ratio: Calculated as total current assets divided by total current liabilities.

As of Dec 31, 2024: $12.495B / $12.797B = 0.98x.

As of Mar 31, 2025: $12.206B / $12.407B = 0.98x.

Working Capital: (Current Assets - Current Liabilities)

As of Dec 31, 2024: $(302) million.

As of Mar 31, 2025: $(201) million. The negative working capital and current ratio below 1.0x warrant monitoring, although common for companies with significant short-term deferred revenue or efficient inventory management. Teva's access to credit facilities and ongoing cash generation are important mitigants.

Table 4: Key Balance Sheet Metrics (FY 2020-2024 Year-Ends, Q1 2025)

(Values in USD millions)

5. Cash Flow Statement

Teva's cash flow statements provide insights into its ability to generate cash from operations, fund its investments, and manage its financing obligations.

Operating Cash Flow (OCF) Analysis

Net cash provided by operating activities was $1.247 billion in FY 2024, compared to $1.368 billion in FY 2023 and $1.590 billion in FY 2022. This declining trend in OCF over the past three full years, despite recent revenue growth, warrants attention. It may be influenced by factors such as the timing of large payments (e.g., for legal settlements, which have been significant for Teva), changes in working capital, or the non-cash components of net income (loss) such as large impairment charges in prior periods that might have inflated OCF then. For Q1 2025, Teva reported cash flow used in operating activities of $105 million, compared to cash flow provided by operating activities of $21 million in Q1 2024. Quarterly OCF can be volatile due to seasonality and timing of payments.

Capital Expenditures (CapEx)

Capital expenditures were $498 million in FY 2024, $526 million in FY 2023, and $548 million in FY 2022. These investments are primarily for purchases of property, plant, and equipment. In Q1 2025, CapEx was $212 million. The level of CapEx is important for maintaining and expanding Teva's manufacturing capabilities and supporting its R&D infrastructure.

Free Cash Flow (FCF)

Free cash flow, calculated as net cash provided by operating activities less capital expenditures, was $749 million in FY 2024. This compares to $842 million in FY 2023 and $1.042 billion in FY 2022.

In Q1 2025, Teva reported free cash flow of $107 million. The company's 2025 full-year FCF outlook is $1.6 - $1.9 billion.

Teva has set ambitious long-term FCF targets: over $2.7 billion in 2027 and over $3.5 billion by 2030. The achievement of these significantly higher FCF levels is heavily reliant on the successful commercialization of its innovative pipeline products, realization of targeted operating margin improvements, and sustained contributions from its generics business. This projected FCF is fundamental to Teva's plans for continued deleveraging and will provide the financial capacity for future strategic investments, whether in R&D, business development, or shareholder returns. Failure to meet these FCF targets would likely impede its ability to reduce debt to the 2x net leverage goal and could constrain its strategic options.

6. Ratio & Trend Analysis

Leverage Ratios

Debt-to-Equity: As of Dec 31, 2024, this was 3.31x. As of Mar 31, 2025, it improved to 2.95x.

Net Debt-to-Adjusted EBITDA: Teva targets reducing this to 2x. As of Q1 2025, Teva reported Net Debt of $14.3 billion and guided for FY2025 Adjusted EBITDA of $4.7-$5.0 billion. Using the midpoint of EBITDA guidance ($4.85B), the pro-forma Net Debt/Adjusted EBITDA is around 2.95x. Continued EBITDA growth and debt paydown are crucial to meet the 2x target.

7. Footnotes & Disclosures (Primarily from latest 10-K and 10-Q)

Key Accounting Policies and Estimates

Teva's financial reporting relies on several critical accounting policies and estimates that can significantly impact its reported results. These include:

Revenue Recognition: Policies for recognizing revenue from product sales, including considerations for rebates, chargebacks, and returns, particularly complex in the U.S. generics market.

Goodwill and Intangible Asset Valuation and Impairment Testing: Given the substantial carrying amounts of goodwill and intangible assets from past acquisitions, the assumptions used in their initial valuation and subsequent impairment testing (e.g., discount rates, growth rates for projected cash flows) are critical. Teva has a history of material impairment charges.

Provisions for Legal Settlements and Contingencies: Estimating liabilities for ongoing legal matters, such as opioid litigation and patent disputes, involves significant judgment regarding the likelihood and potential magnitude of outflows.

Significant Risk Factors and Contingencies

The "Risk Factors" section of the 10-K provides a detailed overview of the challenges and uncertainties Teva faces. Key risks include:

Opioid Litigation: While Teva has reached nationwide settlement agreements to resolve a substantial portion of its opioid-related litigation, the financial impact of these settlements and any remaining exposure continue to be relevant.

Patent Challenges and Loss of Exclusivity: Teva's innovative products are subject to patent protection, and the loss of exclusivity due to patent expiry or successful challenges can lead to rapid revenue declines from generic or biosimilar competition. Conversely, its generics business benefits from such expiries for originator products.

Pricing Pressures in the Generics Market: The generics industry is characterized by intense price competition, consolidation among purchasers, and government pressures to reduce healthcare costs, all of which can impact Teva's revenues and margins in this segment.

Execution Risks of the "Pivot to Growth" Strategy: The success of this strategy depends on numerous factors, including the successful development and commercialization of pipeline products, achieving targeted sales for innovative drugs, realizing planned cost savings, and effectively managing the divestiture of non-core assets like the API business. The 10-K's articulation of these risks highlights management's own assessment of potential hurdles.

Debt and Refinancing Risks: Teva's significant indebtedness requires ongoing management of its debt covenants, interest payments, and refinancing needs.

Geopolitical Risks: As an Israeli-domiciled company with global operations, Teva is exposed to various geopolitical risks.

One-Time Items, Restructuring Charges, Impairments

Teva's financial statements have frequently included items such as restructuring charges, asset impairments (goodwill and intangible assets), and legal settlement expenses. For example, cumulative goodwill impairment was approximately $28.3 billion as of March 31, 2024. While often presented as "non-recurring" or adjusted out in non-GAAP metrics, the historical frequency and magnitude of such charges suggest that they can reflect ongoing costs of business transformation or challenges in realizing the expected value from past acquisitions. Investors should carefully consider both GAAP and non-GAAP results to gain a complete picture of underlying profitability and the true costs associated with Teva's strategic shifts.

Market Positioning

Generics: Teva remains one of the largest generic pharmaceutical companies globally, with a broad portfolio and extensive market reach. However, this market is characterized by intense competition and pricing pressure.

Innovative Portfolio: The strength of Teva's innovative portfolio, particularly AUSTEDO, AJOVY, and UZEDY, and the potential of its late-stage pipeline (duvakitug, olanzapine LAI) are critical differentiators. Benchmarking the R&D productivity—measured by factors such as the number of new drug approvals, progression of pipeline candidates, and sales generated from new products—against peers will be vital in evaluating the effectiveness of its "Stepping up Innovation" pillar. If Teva can successfully transition a greater portion of its revenue mix towards these innovative products, its overall margin profile and growth trajectory could significantly improve relative to more generics-focused competitors.

The ability to achieve its 30% operating margin target will be a key indicator of Teva's transformation. If successful, this would likely elevate its financial profile, potentially leading to a re-rating of its valuation multiples more in line with companies that have a stronger branded pharmaceutical component.

9. Qualitative Aspects

Management Discussion & Analysis (MD&A) Insights

Reviewing management's commentary in the MD&A sections of the 2024 10-K and Q1 2025 10-Q offers direct insights into their perspective on recent performance, the progress of the "Pivot to Growth" strategy, prevailing challenges, and the outlook for key products and segments. Management consistently emphasizes the positive momentum in innovative products and the stabilization of the generics business as core achievements.

Operational Efficiency Initiatives

A key component of the "Pivot to Growth" strategy is the "Focusing the business" pillar, which includes a targeted program to deliver approximately $700 million in net savings by 2027, after reinvestment in growth initiatives. These savings are expected to come from modernizing the organization and improving operational efficiencies. The planned divestiture of the Teva API business is also part of this initiative, aimed at streamlining operations and allowing for greater capital allocation to core growth areas. The successful execution of these efficiency programs is critical for achieving the targeted 30% operating margin.

Deep Dive into Growth Engines

The "Pivot to Growth" strategy is heavily reliant on the performance of its designated growth engines:

Innovative Portfolio:

AUSTEDO: Continued strong U.S. revenue growth (2024: +34%) and prescription growth are being driven by market penetration in tardive dyskinesia and Huntington's disease chorea. The launch of AUSTEDO XR (once-daily formulation) in May 2023 is expected to further enhance its market position. The path to achieving over $2.5 billion by 2027 and over $3 billion by 2030 appears credible based on current momentum.

AJOVY: This anti-CGRP treatment for migraine prevention is now established in 43 countries, with further launches planned. Its global sales growth (+18% in 2024) reflects its competitive positioning.

UZEDY: As a long-acting injectable (LAI) for schizophrenia, UZEDY has shown rapid uptake since its May 2023 launch, capturing over 60% of the risperidone LAI market share in the U.S..

Pipeline Evaluation: The late-stage pipeline holds significant potential and is a cornerstone of future growth expectations.

Duvakitug (anti-TL1A): Following positive Phase 2b results in Crohn's disease and ulcerative colitis, Phase 3 program initiation is expected in the second half of 2025. With a potential best-in-class profile for inflammatory bowel disease and peak sales potential estimated at $2-$5 billion, duvakitug is a key asset. The collaboration with Sanofi on this asset also provides external validation and shared development costs/risks.

Olanzapine LAI: An NDA filing in the U.S. is anticipated in the second half of 2025. This asset is set to expand Teva's LAI franchise in schizophrenia, which has a combined peak sales target of $1.5-$2.0 billion.

DARI (Dual-action Asthma Rescue Inhaler): Aiming to be a first ICS/SABA combination for adult and pediatric patients, DARI has peak sales potential of approximately $1 billion. Phase 3 enrollment is ongoing.

Emrusolmin: A potential first-in-class treatment for Multiple System Atrophy (MSA), a rare and fatal neurodegenerative disease with no current approved treatments. Peak sales potential is estimated at over $2 billion.

TEV-‘408 (Anti-IL-15 antibody): Granted fast-track designation by the FDA for celiac disease, with peak sales potential exceeding $1 billion. The success of these pipeline assets is paramount. Pharmaceutical R&D is inherently risky, and any delays in clinical trials, unfavorable data, or regulatory setbacks could significantly impact Teva's growth projections and investor sentiment.

Generics & Biosimilars Strategy: Teva aims to sustain its "Generics Powerhouse" by focusing on complex generics and biosimilars. The company has 13 biosimilars in its pipeline, with five new launches anticipated by 2027. A key strategic objective is to offset the expected decline in revenues from generic Revlimid (lenalidomide) by 2027 through these new launches and growth in its existing complex generics and OTC portfolio. The $1.1 billion OTC business is also targeted for expansion, with a focus on strong local and global brands. The ability to successfully execute this defensive strategy in the generics segment is crucial for maintaining stable cash flow, which supports investment in innovative R&D and facilitates debt reduction.

10. Valuation

Discounted Cash Flow (DCF) Analysis

The DCF analysis yields an estimated intrinsic value per share of approximately $22.50.

The DCF valuation is heavily influenced by the anticipated success of Teva's innovative pipeline. The projections incorporate the launch and ramp-up of these new products, which inherently carry clinical and commercialization risks.

Owner Earnings: This suggests a value per share of approximately $25.00.

This Owner Earnings valuation, by focusing on cash available after maintaining existing assets, can offer a more conservative view, particularly if future growth investments (embedded in a full DCF are uncertain.

Relative Valuation

As of June 2025, Teva's stock price was around $17.40.

EV/Adjusted EBITDA (Forward): With an enterprise value of approximately $31.7 billion ($17.40 * 1.131B shares + $14.3B net debt) and midpoint 2025 Adjusted EBITDA guidance of $4.85 billion, the forward EV/EBITDA is around 6.5x. This multiple is generally below those of specialty pharmaceutical companies with strong innovative portfolios and growth, suggesting a degree of market skepticism or that the turnaround is not fully priced in. Typical mature pharma EV/EBITDA can range from 8-12x.

5-Year Forward Internal Rate of Return (IRR) Projection

Projected FCF per share (FCF/share):

Year 1 (2025): $1.75B (mid-guidance) / 1.131B shares = $1.55

Year 2 (2026): Growing towards $2.7B target by 2027, assume $2.2B FCF = $1.95/share

Year 3 (2027): $2.7B FCF (target) = $2.39/share

Year 4 (2028): Assume $3.0B FCF = $2.65/share

Year 5 (2029): Assume $3.3B FCF = $2.92/share

Terminal Share Price (Year 5 - end of 2029):

Assume Year 5 EPS (Non-GAAP) grows to ~$3.50 (from 2025's $2.50, reflecting margin expansion and new product contributions).

Apply a terminal P/E multiple of 10x (conservative for a more stable, higher-margin Teva).

Terminal Share Price = $3.50 * 10 = $35.00.

IRR Calculation: Based on an initial investment at $17.40/share and the stream of FCF/share plus the terminal share price:

CF0 = -$17.40

CF1 = $1.55

CF2 = $1.95

CF3 = $2.39

CF4 = $2.65

CF5 = $2.92 (FCF) + $35.00 (Terminal Value) = $37.92

The calculated IRR is approximately 18.5%.

An IRR of this level suggests attractive potential returns if Teva successfully executes its strategy and achieves these FCF and earnings projections.

11. Findings

Teva Pharmaceutical Industries Ltd. is at a pivotal juncture, actively reshaping its business from a generics-dominant entity to a more balanced biopharmaceutical company with significant growth ambitions in innovative medicines. The "Pivot to Growth" strategy, now in its "Acceleration Phase," is the linchpin of this transformation.

Overall Financial Health Assessment

Teva's financial health is showing signs of improvement, though challenges persist.

Strengths: The company has demonstrated a return to revenue growth, driven by the strong uptake of its key innovative products—AUSTEDO, AJOVY, and UZEDY. Non-GAAP operating margins are expanding, and there is a clear path towards the 30% target by 2027. Proactive debt management has led to a reduction in total debt and improved credit ratings from agencies like Moody's and Fitch, enhancing financial flexibility. The generics business, while facing market pressures, has stabilized and continues to generate cash.

Weaknesses: A significant debt load remains on the balance sheet, requiring continued diligent management and substantial free cash flow generation for servicing and reduction. The company has a history of large impairment charges related to past acquisitions, and substantial goodwill and intangible assets still represent a risk. GAAP profitability has been inconsistent, with recent years showing net losses, partly due to these impairments and legal settlements.

Evaluation of Growth & Sustainability

The "Pivot to Growth" strategy is showing encouraging early results.

The innovative portfolio is the primary driver of current growth, with AUSTEDO, AJOVY, and UZEDY performing strongly and expected to continue their trajectory. The sustainability of this growth depends on continued market penetration, successful lifecycle management (e.g., AUSTEDO XR), and fending off eventual competition.

The late-stage pipeline, featuring assets like duvakitug (anti-TL1A for IBD) and olanzapine LAI (for schizophrenia), holds the potential for substantial future revenue streams and margin expansion. The clinical and regulatory success of these assets is paramount for achieving Teva's long-term growth targets of over $5 billion in innovative medicines revenue by 2030 and overall FCF exceeding $3.5 billion by 2030.

The generics business aims to remain a "powerhouse" by focusing on complex generics, biosimilars (with 13 in the pipeline and 5 launches expected by 2027), and expanding its OTC segment. This strategy is crucial for offsetting revenue erosion from older products (like generic Revlimid post-2027) and providing stable cash flow.

Achieving the 2027 and 2030 financial targets (30% operating margin, >$2.7B FCF in 2027, >$3.5B FCF in 2030, 2x net leverage) is ambitious but appears feasible if the innovative pipeline delivers and operational efficiencies are realized.

Future Outlook and Perspective

Teva is navigating a complex but potentially rewarding transformation. The shift towards innovation is strategically sound in an environment where undifferentiated generics face continuous pressure. The current management team, under CEO Richard Francis, has instilled a clear strategic direction and has, thus far, delivered on initial commitments, such as returning the company to top-line growth.

The investment case for Teva hinges on continued successful execution. Positive momentum in the innovative portfolio must be sustained, and the late-stage pipeline must deliver on its promise. Simultaneously, the generics business needs to effectively manage competitive pressures and contribute stable cash flows. Deleveraging remains a key priority and will be facilitated by improved profitability and FCF generation.

If Teva can successfully navigate these elements, there is a clear path to a more profitable, higher-growth company with a stronger balance sheet. However, the pharmaceutical industry is fraught with risks, including clinical trial failures, regulatory hurdles, and intense competition. The market appears to be cautiously optimistic, as reflected in recent stock performance and credit upgrades, but a full re-rating likely awaits further tangible evidence of sustained strategic success and pipeline delivery.

12. Conclusion

Investment Thesis: BUY

Teva Pharmaceutical Industries Ltd. presents a compelling investment opportunity for investors with a medium to long-term horizon. The company is in the midst of a credible turnaround driven by its "Pivot to Growth" strategy, which is showing tangible early successes in revenue growth and margin improvement. The current valuation, with a forward P/E around 7x and EV/EBITDA around 6.5x, does not appear to fully reflect the potential for earnings expansion and free cash flow generation if strategic targets are met. The DCF intrinsic value of ~$22.50, Owner Earnings valuation around ~$25.00, and a projected 5-year IRR of ~18.5% suggest significant upside from the current share price (around $17.40 as of late May 2025).

The investment thesis is predicated on:

Continued strong performance of key innovative growth drivers: AUSTEDO, AJOVY, and UZEDY.

Successful clinical development, regulatory approval, and commercial launch of high-potential pipeline assets, particularly duvakitug and olanzapine LAI.

Achievement of targeted operational efficiencies and cost savings, leading to the 30% non-GAAP operating margin goal by 2027.

Sustained cash flow generation from the generics and biosimilars business.

Progressive deleveraging towards the 2x net debt/EBITDA target.

Key Catalysts to Monitor:

Quarterly earnings reports, focusing on innovative product sales growth, margin progression, and FCF generation.

Clinical trial readouts for duvakitug (Phase 3 initiation H2 2025, future data) and olanzapine LAI (NDA submission H2 2025, approval).

Progress on biosimilar launches and their market uptake.

Updates on the API business divestiture.

Continued progress on debt reduction and achievement of leverage targets.

Key Risks and Potential Catalysts

Downside Risks:

Pipeline Failures: Negative clinical trial results or regulatory rejection for key pipeline assets would severely impact future growth prospects.

Intensified Competition: Greater-than-expected price erosion in generics or stronger competition for innovative products could undermine revenue and margin targets.

Execution Missteps: Failure to achieve planned cost savings or effectively manage the complexities of a global business transformation.

Debt Burden: While improving, a significant downturn in performance could strain Teva's ability to service and reduce its debt.

Macroeconomic Factors: Currency fluctuations, changes in healthcare policy, or geopolitical instability could adversely affect operations.

Upside Catalysts:

Positive Phase 3 Data/Approvals: Strong efficacy and safety data for duvakitug or olanzapine LAI, leading to successful approvals and launches.

Accelerated Growth of In-Market Innovatives: AUSTEDO, AJOVY, or UZEDY exceeding sales expectations.

Successful New Biosimilar Launches: Capturing significant market share with new biosimilar products.

Achieving Financial Targets Ahead of Schedule: Faster-than-anticipated margin expansion or FCF generation.

Further Credit Rating Upgrades: Leading to lower cost of debt and broader investor appeal.

Strategic Business Development: Value-accretive acquisitions or partnerships that enhance the innovative pipeline or specialty portfolio.

In conclusion, Teva Pharmaceutical Industries Ltd. offers an attractive risk/reward profile for investors willing to underwrite the execution of its strategic transformation. The path forward involves navigating inherent industry challenges, but the potential for value creation is substantial if the "Pivot to Growth" continues to yield positive results.